All Categories

Featured

Table of Contents

- – Who offers flexible Low Cost Level Term Life I...

- – Why do I need Best Level Term Life Insurance?

- – How do I choose the right Level Term Life Ins...

- – Can I get Level Term Life Insurance For Senio...

- – How long does Level Premium Term Life Insura...

- – Can I get Level Term Life Insurance Benefits...

Costs are normally lower than entire life policies. With a level term policy, you can choose your insurance coverage amount and the plan length.

And you can not squander your plan throughout its term, so you will not obtain any kind of economic take advantage of your past protection. As with other types of life insurance, the cost of a level term plan relies on your age, protection needs, employment, lifestyle and wellness. Normally, you'll discover much more cost effective protection if you're more youthful, healthier and less dangerous to insure.

Considering that level term premiums remain the same throughout of protection, you'll understand precisely how much you'll pay each time. That can be a big assistance when budgeting your costs. Degree term protection likewise has some flexibility, allowing you to personalize your plan with added functions. These commonly can be found in the type of bikers.

You might have to fulfill particular conditions and qualifications for your insurance company to enact this rider. There also could be an age or time restriction on the coverage.

Who offers flexible Low Cost Level Term Life Insurance plans?

The survivor benefit is typically smaller, and coverage usually lasts till your kid turns 18 or 25. This motorcyclist may be a more cost-effective method to aid ensure your kids are covered as riders can usually cover multiple dependents at the same time. Once your youngster ages out of this insurance coverage, it may be feasible to transform the biker right into a new policy.

When contrasting term versus irreversible life insurance, it is very important to keep in mind there are a couple of different kinds. One of the most common kind of irreversible life insurance policy is whole life insurance policy, however it has some vital differences compared to level term protection. Below's a basic overview of what to take into consideration when comparing term vs.

Whole life insurance lasts for life, while term protection lasts for a certain period. The costs for term life insurance coverage are commonly less than whole life insurance coverage. Nevertheless, with both, the premiums stay the same for the duration of the plan. Whole life insurance policy has a cash money worth component, where a section of the costs may expand tax-deferred for future requirements.

Why do I need Best Level Term Life Insurance?

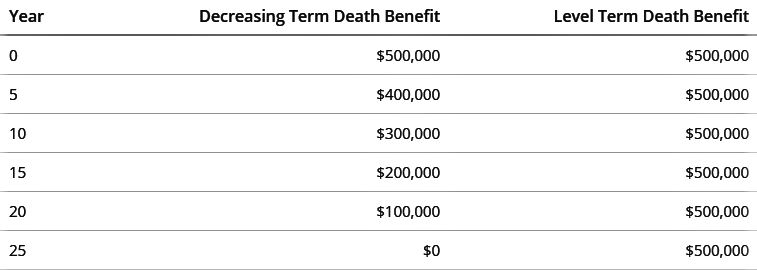

One of the primary functions of degree term protection is that your costs and your fatality advantage don't change. You might have coverage that starts with a death benefit of $10,000, which can cover a home loan, and then each year, the fatality advantage will reduce by a collection quantity or percent.

Due to this, it's usually a much more cost effective type of degree term insurance coverage., yet it may not be enough life insurance coverage for your demands.

After determining on a plan, complete the application. If you're accepted, authorize the documentation and pay your first premium.

Consider scheduling time each year to examine your plan. You might wish to update your recipient details if you've had any type of substantial life adjustments, such as a marital relationship, birth or separation. Life insurance policy can often feel complex. You don't have to go it alone. As you discover your choices, think about reviewing your demands, desires and worries with a monetary specialist.

How do I choose the right Level Term Life Insurance For Families?

No, level term life insurance policy doesn't have cash value. Some life insurance policy plans have a financial investment attribute that allows you to build money value with time. What is level term life insurance?. A section of your costs settlements is set aside and can earn rate of interest with time, which grows tax-deferred throughout the life of your protection

These plans are usually substantially extra expensive than term coverage. You can: If you're 65 and your coverage has actually run out, for example, you might want to buy a new 10-year degree term life insurance plan.

Can I get Level Term Life Insurance For Seniors online?

You might be able to convert your term protection right into a whole life policy that will certainly last for the remainder of your life. Lots of kinds of level term policies are exchangeable. That means, at the end of your insurance coverage, you can convert some or every one of your policy to entire life coverage.

Degree term life insurance policy is a policy that lasts a collection term typically in between 10 and three decades and includes a degree death advantage and level costs that stay the very same for the whole time the plan is in effect. This means you'll understand exactly just how much your repayments are and when you'll have to make them, allowing you to budget plan as necessary.

Level term can be a great choice if you're looking to get life insurance policy protection for the first time. According to LIMRA's 2023 Insurance coverage Barometer Research, 30% of all grownups in the U.S. demand life insurance coverage and do not have any sort of policy yet. Degree term life is predictable and budget-friendly, which makes it one of the most popular types of life insurance policy

A 30-year-old male with a similar profile can anticipate to pay $29 each month for the very same insurance coverage. AgeGender$250,000 insurance coverage quantity$500,000 coverage amount$1 million insurance coverage amount20Female$15$23$34Male$19$29$4830Female$15$23$37Male$18$29$4940Female$22$35$61Male$25$43$7550Female$44$78$139Male$57$102$18860Female$108$194$355Male$149$268$500 Collapse table Technique: Ordinary regular monthly prices are calculated for male and women non-smokers in a Preferred health and wellness category obtaining a 20-year $250,000, $500,000, or $1,000,000 term life insurance coverage policy.

How long does Level Premium Term Life Insurance coverage last?

Rates may vary by insurer, term, coverage amount, health class, and state. Not all policies are available in all states. Price picture valid as of 09/01/2024. It's the cheapest type of life insurance for lots of people. Degree term life is far more budget-friendly than a similar whole life insurance policy plan. It's easy to handle.

It permits you to budget plan and strategy for the future. You can quickly factor your life insurance policy into your budget plan because the costs never ever transform. You can prepare for the future simply as conveniently because you understand precisely just how much money your liked ones will certainly obtain in the occasion of your lack.

Can I get Level Term Life Insurance Benefits online?

This is real for individuals who stopped smoking or who have a health condition that solves. In these situations, you'll usually need to go with a brand-new application process to get a better rate. If you still require coverage by the time your level term life plan nears the expiry date, you have a couple of alternatives.

{kind=link}

Table of Contents

- – Who offers flexible Low Cost Level Term Life I...

- – Why do I need Best Level Term Life Insurance?

- – How do I choose the right Level Term Life Ins...

- – Can I get Level Term Life Insurance For Senio...

- – How long does Level Premium Term Life Insura...

- – Can I get Level Term Life Insurance Benefits...

Latest Posts

Buy Funeral Cover Online

No Exam Instant Life Insurance

Affordable Funeral Insurance Plans

More

Latest Posts

Buy Funeral Cover Online

No Exam Instant Life Insurance

Affordable Funeral Insurance Plans